TOKYO, Dec 8 (Reuters) – International buyers are short-selling Japanese bonds and driving its different market yields larger, reviving bets that the Financial institution of Japan might want to tweak its ultra-easy financial coverage sooner moderately than later.

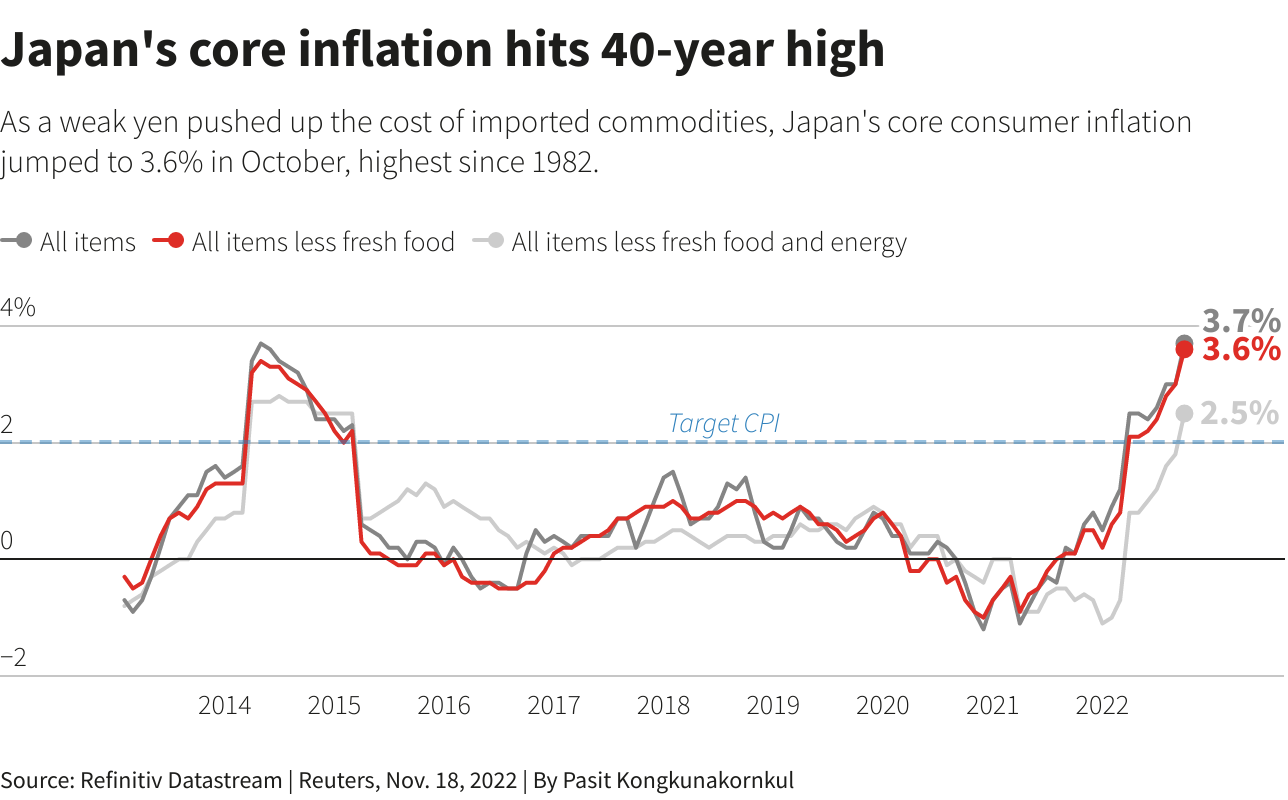

The wagers have perked up after information late final month confirmed shopper costs in Tokyo rose at their quickest annual tempo in 40 years in November, suggesting the BOJ could be nearer to attaining its coverage intent of sustained 2% inflation.

“With costs rising, hypothesis that the Financial institution of Japan could change its yield curve management is getting stronger than earlier than,” mentioned Masayuki Koguchi, common supervisor on the mounted earnings funding division of Mitsubishi UFJ Kokusai Asset Administration.

The bets have saved yields on benchmark 10-year bonds at 0.25% — the highest finish of the BOJ’s goal band — for days, even because the central financial institution continues to supply to purchase limitless quantities of bonds with that maturity. Entrance-end swaps present 3-month charges turning constructive by February.

BOJ Governor Haruhiko Kuroda has repeatedly harassed the necessity to stick with the financial institution’s distinctive yield-curve-control coverage, which makes Japan an outlier amongst main central banks aggressively tightening coverage to fight inflation.

Underneath its yield curve management (YCC), the BOJ guides short-term rates of interest at -0.1% and pledges to information the 10-year bond yield round 0% with an implicit 0.25% cap.

“The main focus simply on the 10-year yield and YCC is a bit bizarre as a result of the remainder of the charges market has already fully moved on from YCC,” mentioned UBS’s London-based strategist James Malcolm, pointing to how 10-year swaps used to straddle the JGB yield till early this 12 months and are actually greater than double the worth at 63 foundation factors (bps).

Kuroda has mentioned coverage won’t change till the current cost-push inflation is accompanied by larger development in wages. That, and a suspicion Kuroda will keep away from making modifications within the remaining months of his time period that ends in early April, has derailed buyers betting on a change a number of instances this 12 months.

“Brief positions on JGBs haven’t been lined but,” mentioned Ataru Okumura, a strategist at SMBC Nikko Securities.

Foreigners have offered 1.1 trillion yen ($8.02 billion) of JGBs within the week ended Dec. 3, which adopted 45.1 billion yen of promoting within the earlier week.

WAGE TALKS

The divergence between the BOJ’s dovish stance and the U.S. Federal Reserve’s aggressive fee hikes had pushed the yen to 32-year lows in October.

“The central financial institution could tweak its YCC earlier than March. The choice could possibly be made after the ‘shunto’, however the BOJ could not have to attend for that,” mentioned Ayako Fujita, chief Japan economist at JPMorgan Securities.

The “shunto” spring wage talks occur each March, when Japan’s blue-chip corporations meet with unions to debate staff’ pay within the subsequent fiscal 12 months.

A identified BOJ dove and board member Asahi Noguchi mentioned final week the central financial institution might “pre-emptively” withdraw financial stimulus if development inflation, which takes into consideration wage and providers costs, overshoots expectations and stays above its 2% goal.

Merchants additionally pointed to remarks from Naoki Tamura, a brand new BOJ board member, saying the Financial institution ought to study the professionals and cons of yield curve management and that the coverage had prompted market mispricing, as the newest purpose for the hypothesis.

The BOJ might increase its goal for 10-year yield from 0 to 25 bps, or widen the buying and selling band by 25 bps to 0.50% on both aspect, mentioned Fujita.

The BOJ’s subsequent coverage conferences are on Dec. 19-20, after which on Jan. 17-18.

Kuroda’s current speeches on the framework for exiting straightforward financial situations have been centred round short-term charges and the BOJ’s burgeoning stability sheet, giving speculators additional purpose to imagine he’s not wedded to YCC per se.

“My private view is that the January assembly is kind of stay as a result of it’s Mr. Kuroda’s final outlook assembly. There needs to be an occasion weight it doesn’t have in the meanwhile,” says Malcolm, whereas making clear UBS doesn’t anticipate any coverage change for not less than one other 12 months.

($1 = 137.0900 yen)

Reporting by Junko Fujita

Enhancing by Vidya Ranganathan and Kim Coghill

: .